"In the long run, we are all dead."

Life and Contributions of John Maynard Keynes

Major Contributions

Macroeconomics, Keynesian Economics, Liquidity preference, Spending multiplier, Aggregate Demand-Aggregate Supply model

Macroeconomics, Keynesian Economics, Liquidity preference, Spending multiplier, Aggregate Demand-Aggregate Supply model

Early Life

John Maynard Keynes had an enriched childhood as both his father, John Neville Keynes, and mother, Florence Keynes, went to Cambridge and had influential and intellectual occupations.

Keynes entered a career in the Civil Service when he graduated from King’s College in 1905. Later, he resigned his position in the government and began teaching and writing on economic issues. In 1911, Keynes became the editor of the Economic Journal in 1911 and published his first book Indian Currency and Finance in 1913, which was based on what he lectured at the London School of Economics.

During WWI

Keynes joined the British Treasury Department of the Civil Service, which was to deal with the financial side of war. Bertrand Russell claimed that Keynes' work at the Treasury "consisted of finding ways of killing the maximum number of Germans at the minimum expense".' As the war ended, Keynes was sent as part of the British delegation to the Versailles Peace Conference of 1919. However, he ended up being disappointed by the result of the conference and wrote The Economic Consequences of the Peace to express his opinions.

During the Great Depression

When the Depression hit, Keynes, as the chairman of the Economic Advisory Council, published his report on "the causes and remedies of the depression.” In the committee formed to deal with Britain’s economic problems in March 1931, Keynes suggested that the best way to deal with the crisis was to leave the gold standard. However, the committee ended without a conclusion.

Keynes was extremely active in his campaign to encourage the government to take more responsibility for running the economy. In 1936, Keynes published his most important book, A General Theory of Employment, Interest and Money, which included his views on the planned economy that influenced President Franklin D. Roosevelt. The book was also a factor in the introduction of the New Deal as well as the economic policies of Britain's post-war Labour Government.

During WWII

Keynes was then an unpaid advisor to the Chancellor of the Exchequer. In 1940, he wrote the influential How to Pay for the War. He attended the Bretton Woods Conference in 1944 and the Savannah Conference in 1946. He was also involved in the negotiations on Lend-Lease and the US loan to Britain.

On April 21st, 1946, Keynes died form a heart attack.

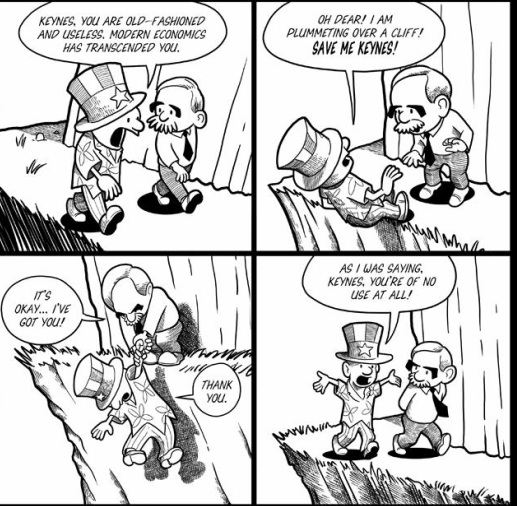

"What Keynes' General Theory did, was to throw economists into two violently opposed camps. However, as it turned out, and principally because of its appeal to free spending politicians, the Keynesians, up to the 1980s, were to have their way. The fact is, that Keynesian economics applied during good times, bring on bad times."

John Maynard Keynes had an enriched childhood as both his father, John Neville Keynes, and mother, Florence Keynes, went to Cambridge and had influential and intellectual occupations.

Keynes entered a career in the Civil Service when he graduated from King’s College in 1905. Later, he resigned his position in the government and began teaching and writing on economic issues. In 1911, Keynes became the editor of the Economic Journal in 1911 and published his first book Indian Currency and Finance in 1913, which was based on what he lectured at the London School of Economics.

During WWI

Keynes joined the British Treasury Department of the Civil Service, which was to deal with the financial side of war. Bertrand Russell claimed that Keynes' work at the Treasury "consisted of finding ways of killing the maximum number of Germans at the minimum expense".' As the war ended, Keynes was sent as part of the British delegation to the Versailles Peace Conference of 1919. However, he ended up being disappointed by the result of the conference and wrote The Economic Consequences of the Peace to express his opinions.

During the Great Depression

When the Depression hit, Keynes, as the chairman of the Economic Advisory Council, published his report on "the causes and remedies of the depression.” In the committee formed to deal with Britain’s economic problems in March 1931, Keynes suggested that the best way to deal with the crisis was to leave the gold standard. However, the committee ended without a conclusion.

Keynes was extremely active in his campaign to encourage the government to take more responsibility for running the economy. In 1936, Keynes published his most important book, A General Theory of Employment, Interest and Money, which included his views on the planned economy that influenced President Franklin D. Roosevelt. The book was also a factor in the introduction of the New Deal as well as the economic policies of Britain's post-war Labour Government.

During WWII

Keynes was then an unpaid advisor to the Chancellor of the Exchequer. In 1940, he wrote the influential How to Pay for the War. He attended the Bretton Woods Conference in 1944 and the Savannah Conference in 1946. He was also involved in the negotiations on Lend-Lease and the US loan to Britain.

On April 21st, 1946, Keynes died form a heart attack.

"What Keynes' General Theory did, was to throw economists into two violently opposed camps. However, as it turned out, and principally because of its appeal to free spending politicians, the Keynesians, up to the 1980s, were to have their way. The fact is, that Keynesian economics applied during good times, bring on bad times."

Major Publications and Ideas

The Economic Consequences of the Peace (1919)

Keynes’ wrote eloquently and passionately of his objection to the heavy reparations imposed on Germany after World War I at the Treaty of Versailles. This book launched Keynes to global fame. He argued that the reparations were so heavy that they would devastate the German economy, keeping Germany perpetually impoverished and harming innocent German people. Germany’s ability to buy exports from other countries was also limited, and Germany would be politically unstable. Therefore, all of Europe would be threatened.

A Tract on Monetary Reform (1923)

Treatise on Money (1930)

Both works deal with monetary policy. Keynes became increasingly preoccupied with two forms of economic stability, the instability of prices, which inflated and deflated, and unemployment. His main view was that to stabilize the economy, prices had to be stabilized, and that to do so, the government’s central bank had to lower interest rates when prices rose and raise interest rates when prices fell. In A Tract on Monetary Reform, Keynes argued that deflation had to be avoided even if currency were to depreciate. A depreciation of the British currency could give rise to more jobs by making British exports more affordable. This directly went against the gold standard Britain favored at the time. In Treatise on Money, Keynes argued that if the amount of money being saved was greater than the amount of money being invested in the economy, unemployment would rise because people are hoarding their money instead of pumping it into the economy. Businesses, the employers, won’t be able to make a profit and therefore can’t hire. People may be induced to save instead of spend because interest rates are too high, and therefore, the government should set interest rates to adjust the economy.

A General Theory of Employment, Interest, and Money (1936)

This was Keynes most important and revolutionary book. It challenged traditional ideas about the “invisible hand” that a free market without government interference would naturally result in full employment because workers will always lower wages to find work and employers can earn a profit. Keynes argued that the classic theory was a special case. Humans are not all rational as classical economists assume. Sometimes, there is price stickiness. That is, the workers refuse to lower wages when it is rational for them to do so. Aggregate demand, the total un-hoarded income in a society, should be the focus of economic policies. Aggregate demand (money available for earning) is the sum of consumption and investment. When there is unemployment, people are not spending as much money. Businesses do not make as many products, leaving many factors of production unused. Because businesses do not make as much money, they do not hire as many people. It’s a vicious low employment cycle. To break the cycle, the government must interfere, spending money into the economy. Government stimulus such as spending money on public projects create more jobs, giving people more money to spend, and giving businesses more money to produce and therefore more money to hire. Therefore, when the economy is in a slump and unemployment rates are high, the government must run a deficit investing into the economy.

Keynes’ wrote eloquently and passionately of his objection to the heavy reparations imposed on Germany after World War I at the Treaty of Versailles. This book launched Keynes to global fame. He argued that the reparations were so heavy that they would devastate the German economy, keeping Germany perpetually impoverished and harming innocent German people. Germany’s ability to buy exports from other countries was also limited, and Germany would be politically unstable. Therefore, all of Europe would be threatened.

A Tract on Monetary Reform (1923)

Treatise on Money (1930)

Both works deal with monetary policy. Keynes became increasingly preoccupied with two forms of economic stability, the instability of prices, which inflated and deflated, and unemployment. His main view was that to stabilize the economy, prices had to be stabilized, and that to do so, the government’s central bank had to lower interest rates when prices rose and raise interest rates when prices fell. In A Tract on Monetary Reform, Keynes argued that deflation had to be avoided even if currency were to depreciate. A depreciation of the British currency could give rise to more jobs by making British exports more affordable. This directly went against the gold standard Britain favored at the time. In Treatise on Money, Keynes argued that if the amount of money being saved was greater than the amount of money being invested in the economy, unemployment would rise because people are hoarding their money instead of pumping it into the economy. Businesses, the employers, won’t be able to make a profit and therefore can’t hire. People may be induced to save instead of spend because interest rates are too high, and therefore, the government should set interest rates to adjust the economy.

A General Theory of Employment, Interest, and Money (1936)

This was Keynes most important and revolutionary book. It challenged traditional ideas about the “invisible hand” that a free market without government interference would naturally result in full employment because workers will always lower wages to find work and employers can earn a profit. Keynes argued that the classic theory was a special case. Humans are not all rational as classical economists assume. Sometimes, there is price stickiness. That is, the workers refuse to lower wages when it is rational for them to do so. Aggregate demand, the total un-hoarded income in a society, should be the focus of economic policies. Aggregate demand (money available for earning) is the sum of consumption and investment. When there is unemployment, people are not spending as much money. Businesses do not make as many products, leaving many factors of production unused. Because businesses do not make as much money, they do not hire as many people. It’s a vicious low employment cycle. To break the cycle, the government must interfere, spending money into the economy. Government stimulus such as spending money on public projects create more jobs, giving people more money to spend, and giving businesses more money to produce and therefore more money to hire. Therefore, when the economy is in a slump and unemployment rates are high, the government must run a deficit investing into the economy.

Influence on Field of Economics

The Keynesian Era 1939–1979

From the end of Great Depression to the 1970s, Keynes's ideas provided great inspiration for economis policy makers in most of the developed countries in the world, from European countries to the United States. President Franklin Roosevelt used government funds for public projects, in line with Keynesian economics. As he explained in a fireside chat, "We suffer primarily from a failure of consumer demand because of a lack of buying power." The government had to "create an economic upturn" by making "additions to the purchasing power of the nation." For the next forty or so years, the Federal Government managed the US economy, and it became widely accepted that the government could "fine-tune" the economy by using fiscal and monetary policy. As Richard Nixon famously said, "We are all Keynesians now."

Neo-Keynesian Economics

Neo-Keynesian economics was produced by synthesizing Keynesian analysis and neo-classical economics in the late 1930s-1940s. Notable Neo-Keynesians were John Hicks, Franco Modigliani, and Paul Samuelson. Their work has become known as the neo-classical synthesis. These ideas dominated mainstream economics in the post-war period and formed the mainstream of macroeconomic thought in the 1950s, 60s and 70s.

Out of Favor (1979–2007)

Many models were developed by Keynesian economists, most famously the Phillips curve which predicted an inverse relationship between unemployment and inflation. (It implied that unemployment could be reduced by government stimulus with a calculable cost to inflation.) In 1968 Milton Friedman published a paper arguing that the fixed relationship implied by the Philips curve did not exist.

The phenomenon of stagflation and the rise of monetarists such as Milton Friedman made policy makers and economists start to lose trust in neo-Keynesian theories. British forces began to oppose Keynesian economics in the 1950s. Finally, Keynesian economics were officially discarded by the British Government in 1979.

The Return of Keynes (2008–2009)

The Fiancial crisis of 2007-2010 made people doubt the free market consensus. In March 2008, Martin Wolf, chief economics commentator at the Financial Times, announced the death of the dream of global free-market capitalism. He implied the resurgence of Keynes's ideas of social liberalism. In the same month, macro-economist James K. Galraith made a speech arguing that Keynesian economics were far more relevant for tackling the emerging crises. Economist Robert Shiller had begun advocating robust government intervention to tackle the financial crises, specifically citing Keynes. Nobel laureate Paul Krugman also actively argued the case for vigorous Keynesian intervention in his columns for the New York Times.

From the end of Great Depression to the 1970s, Keynes's ideas provided great inspiration for economis policy makers in most of the developed countries in the world, from European countries to the United States. President Franklin Roosevelt used government funds for public projects, in line with Keynesian economics. As he explained in a fireside chat, "We suffer primarily from a failure of consumer demand because of a lack of buying power." The government had to "create an economic upturn" by making "additions to the purchasing power of the nation." For the next forty or so years, the Federal Government managed the US economy, and it became widely accepted that the government could "fine-tune" the economy by using fiscal and monetary policy. As Richard Nixon famously said, "We are all Keynesians now."

Neo-Keynesian Economics

Neo-Keynesian economics was produced by synthesizing Keynesian analysis and neo-classical economics in the late 1930s-1940s. Notable Neo-Keynesians were John Hicks, Franco Modigliani, and Paul Samuelson. Their work has become known as the neo-classical synthesis. These ideas dominated mainstream economics in the post-war period and formed the mainstream of macroeconomic thought in the 1950s, 60s and 70s.

Out of Favor (1979–2007)

Many models were developed by Keynesian economists, most famously the Phillips curve which predicted an inverse relationship between unemployment and inflation. (It implied that unemployment could be reduced by government stimulus with a calculable cost to inflation.) In 1968 Milton Friedman published a paper arguing that the fixed relationship implied by the Philips curve did not exist.

The phenomenon of stagflation and the rise of monetarists such as Milton Friedman made policy makers and economists start to lose trust in neo-Keynesian theories. British forces began to oppose Keynesian economics in the 1950s. Finally, Keynesian economics were officially discarded by the British Government in 1979.

The Return of Keynes (2008–2009)

The Fiancial crisis of 2007-2010 made people doubt the free market consensus. In March 2008, Martin Wolf, chief economics commentator at the Financial Times, announced the death of the dream of global free-market capitalism. He implied the resurgence of Keynes's ideas of social liberalism. In the same month, macro-economist James K. Galraith made a speech arguing that Keynesian economics were far more relevant for tackling the emerging crises. Economist Robert Shiller had begun advocating robust government intervention to tackle the financial crises, specifically citing Keynes. Nobel laureate Paul Krugman also actively argued the case for vigorous Keynesian intervention in his columns for the New York Times.

RSS Feed

RSS Feed